South Bronx residents have long put up with limited access to financial services in their own neighborhoods. The closing of local bank branches in recent years has made the problem even worse.

One financial collective with branches around the city, however, is hoping to change that, by expanding its reach into the neighborhood, offering services such as free checking and savings accounts, credit builder loans and low-cost auto loans. The People’s Federal Credit Union, which has branches in the Lower East Side, East Harlem, and Staten Island, plans to open a new brick-and-mortar branch somewhere in the South Bronx next year, with the goal of making access to financial services easier for people likely to be turned away from traditional banks.

Members of the collective and South Bronx advocacy groups involved in the project gathered on July 19 at Boricua Community College in Melrose to announce the plans for next year’s branch opening.

Until a permanent site is established, the Credit Union will continue operating a mobile unit at pop-up locations around the borough, with the help of partnering community organizations. As previously reported in The Herald, the idea for a mobile banking van in the Bronx was first introduced in April.

Community groups have tried to get the project off the ground have met with numerous banks to consider ways to overcome the troubling trend of recent closures and start up a new, more accessible alternative. Representatives from the Bronx Financial Access Coalition (BxFac) found a willing sponsor when they met with officials from the Webster Bank (formerly Sterling National Bank), which had closed its branch in The Hub, and Webster bank officials agreed.

Finding a willing partner was not easy, said Jessica Clemente, president and CEO of Melrose community group Nos Quedamos.

“They repeatedly mentioned costs,” said Clemente. “Some were in the process of merging. Webster stepped up and committed the money.”

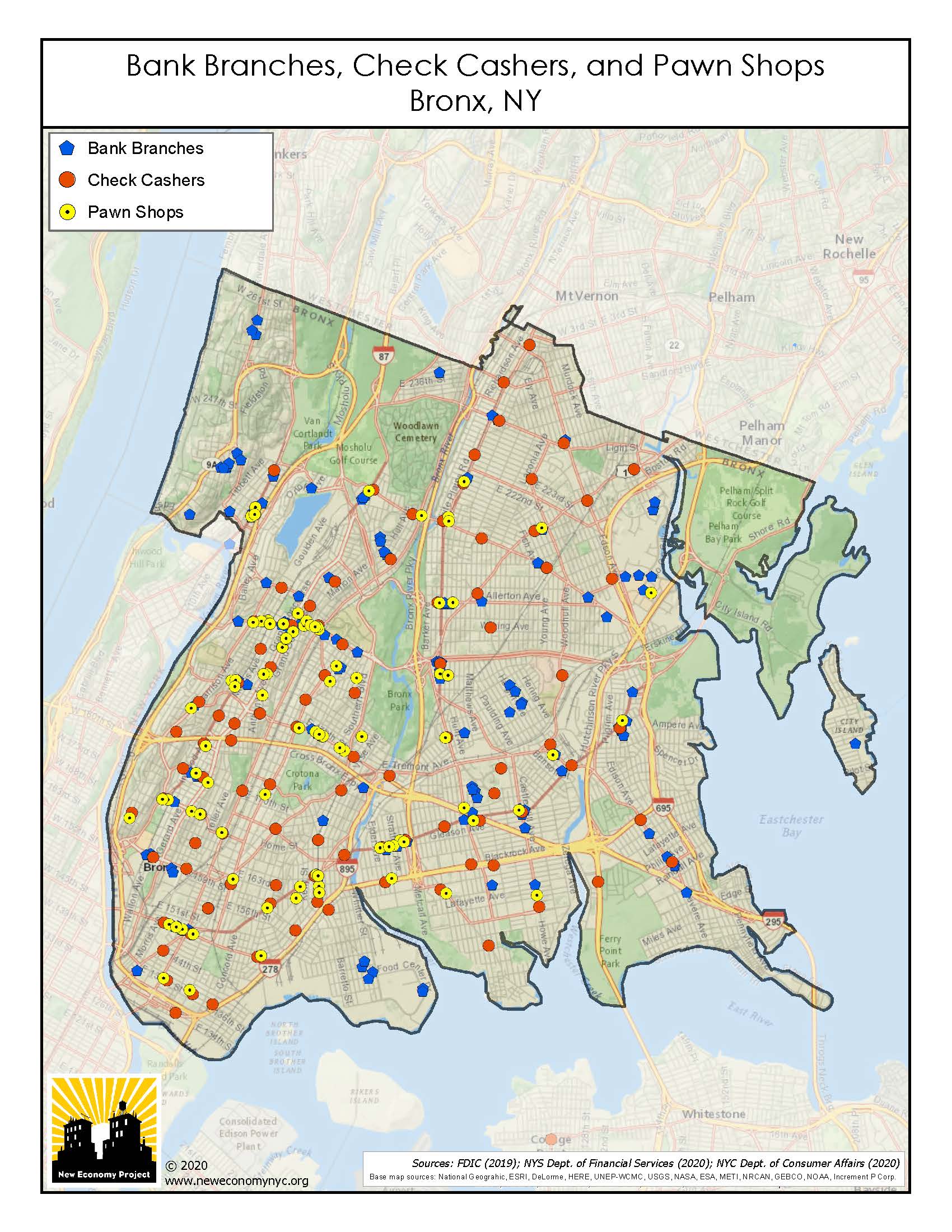

Even before the effects of the pandemic led to yet more South Bronx branches leaving, the Bronx was home to the fewest bank branches in the five boroughs, with the familiar clusters of check cashing places and pawn shops offering only the most basic services, with high fees.

{kind=link}

Among local branches to close recently were Popular Bank, Chase, Amalgamated, and Sterling National (now Webster Bank). Between 2017 and 2022, 33 bank branches closed in the Bronx, and only nine new ones opened, according to the FDIC.

A report by the Association for Neighborhood & Housing Development states that The Bronx has “the highest rates of unbanked and underbanked households, the lowest concentration of bank branches per household, the highest percentages of Black and Latinx residents, and the poorest residents in the city.”

Because the few existing branches are clustered in commercial corridors like The Hub, many residents opt to use check cashing businesses and pawn shops as alternatives.

Melrose resident Sonya Ferguson, 62, who signed up for an account with the credit union through the mobile branch, said fees added up when she used debit cards to do her banking at local check cashing storefronts.

“They told me it was going to be $10,” for the prepaid card, she said. Putting $100 on the card cost her another $5, and by the time she used it at an ATM, she was stunned to find she had racked up almost $20 in fees. When she signed up for an account with the credit union, she was relieved to find there were no such fees.

Kerry McLean, vice president at Women’s Housing and Economic Development Corporation (WHEDco), said her organization conducted a survey of about 400 community members and found that although two thirds of the respondents were employed, only one in four had a bank account.

“Four of 10 [community members] had zero dollars in savings,” McLean added

Clemente hopes that other financial institutions will follow Webster Bank’s lead, seeing the value in returning to a community they recently left and being mindful that not only wealthy neighborhoods need robust banking services.

“There is still an opportunity,” she said. “The door is not closed.”